Homeownership in Cyprus continues to represent both a lifestyle choice and a long-term financial strategy. While mortgage repayments often seem like an unavoidable cost, the true financial picture is more nuanced. A home can function as both a liability and a wealth-building asset — depending on how interest, property appreciation, and time interact. This report explores how these forces shape long-term value for primary homeowners in Cyprus, using recent data on lending rates and housing price trends.

Understanding the Cost of Borrowing

As of mid-2025, Cyprus mortgage rates for primary residences generally range between 3.8% and 4.5%, depending on loan structure and borrower profile. The Central Bank of Cyprus reported an average rate of 3.87% in July 2025, with major lenders such as Bank of Cyprus and Hellenic Bank offering housing loans near 4.3%–4.5%. Fixed-rate options, often at slightly higher margins, provide payment stability during the European Central Bank’s gradual rate adjustments.

Because mortgages in Cyprus are typically amortizing, the interest portion of monthly payments is highest in the early years. Over time, as the outstanding balance declines, a greater share of each installment contributes to equity. On a €240,000 loan at 4.5% over 25 years, the total interest cost can exceed €200,000 – meaning that understanding and managing this cost is critical. Homeowners can mitigate it through shorter loan terms, partial prepayments, or refinancing when rates fall.

Home Value Appreciation and Market Dynamics

On the other side of the equation lies appreciation – the gradual increase in property value over time. Cyprus’ housing market has displayed steady momentum in recent years. According to the Central Bank’s Residential Property Price Index, the index reached 113.71 points in Q1 2025, a 1.1% quarterly and 2.0% annual increase. PwC’s ‘Cyprus Real Estate Market Year in Review 2024’ cited an average 7% rise in residential prices, while CEIC data estimated year‑on‑year growth of 6.5% in September 2024.

Apartments have tended to outperform houses — with recent figures showing 8–9% annual growth for apartments compared to 5-6% for detached homes. Demand remains strong in coastal and urban centers such as Limassol, Larnaca, and Paphos, fueled by population growth, foreign investment, and limited new supply. Although short‑term moderation is expected, the long‑term trajectory for quality housing remains upward.

How Interest and Appreciation Interact Over Time

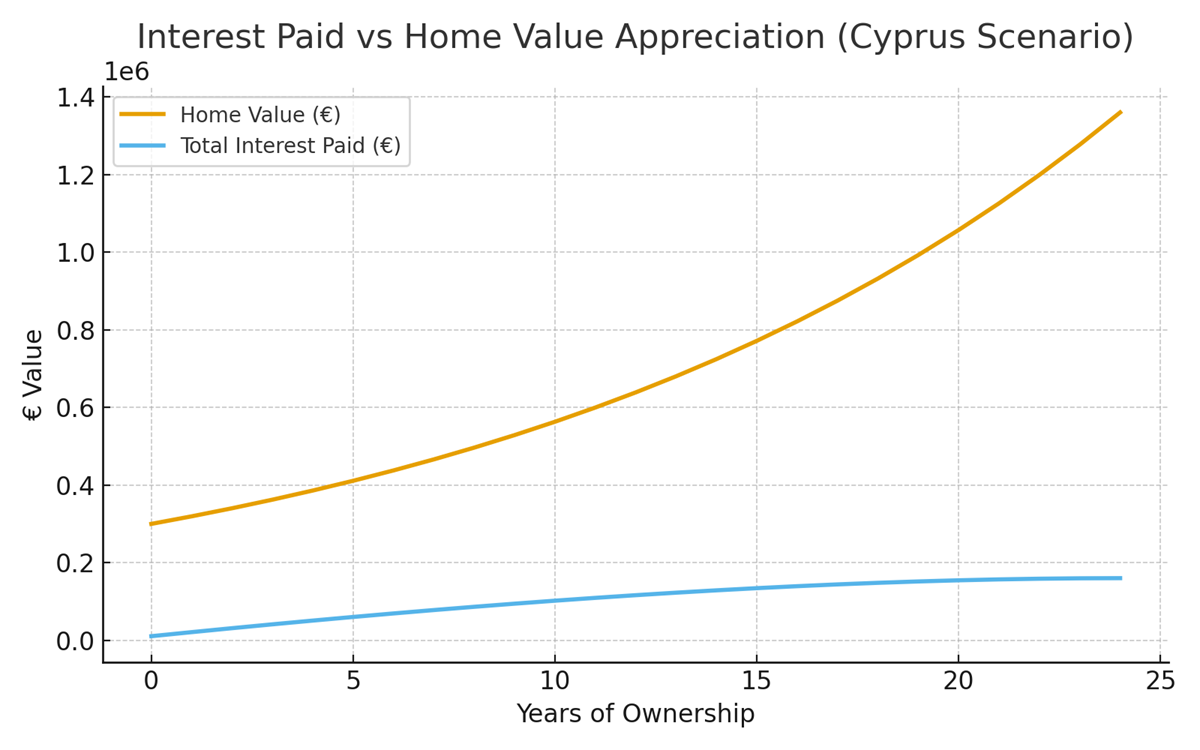

Consider a practical example: a homeowner purchases a €300,000 property with a €240,000 mortgage at 4.5% interest over 25 years. Assuming the property appreciates at 6.5% annually – consistent with recent trends – its value after 20 years would reach roughly €1.07 million. Over the same period, cumulative interest payments total about €200,000, but these payments gradually decline as principal is repaid.

The key insight is that the compounding effect of appreciation often outpaces the drag of interest – especially beyond the first decade of ownership. By year 15, equity gains (from both appreciation and principal repayment) typically surpass cumulative interest costs. Even if appreciation slows to 3%, long‑term owners who stay the course continue to benefit from gradual wealth accumulation and inflation‑adjusted asset growth.

Economic Context and Historical Perspective

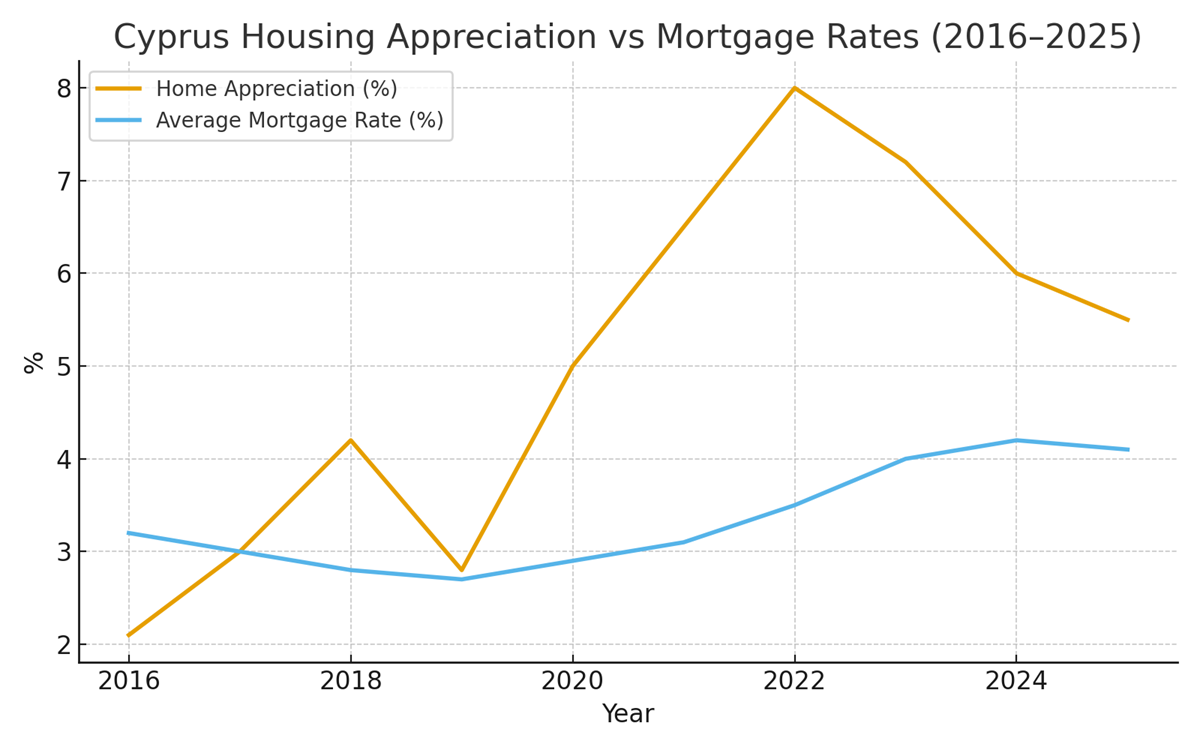

Cyprus’ property market has evolved significantly since the early 2010s financial restructuring. Stable GDP growth, improved lending conditions, and ongoing tourism‑related demand have supported values. The chart below compares annual housing appreciation to average mortgage rates from 2016 to 2025, showing that during most years, appreciation exceeded the cost of borrowing — a favorable environment for leveraged homeowners.

Looking forward, continued alignment with ECB policy and domestic affordability will likely moderate price growth to around 4 – 5% annually, which still compares favorably against expected long‑term borrowing costs. Even in moderate growth environments, homeownership serves as a disciplined, inflation‑hedged savings mechanism.

Key Takeaways for Cypriot Homeowners

- Mortgage rates remain moderate relative to recent inflation, preserving borrowing affordability.

• Historical price appreciation — especially in urban and coastal zones — often exceeds mortgage interest rates over time.

• Long‑term ownership allows equity to compound as interest costs decline and inflation supports nominal price growth.

• Refinancing opportunities and disciplined maintenance help maximize net returns.Ultimately, homeownership in Cyprus remains a powerful tool for long‑term wealth building. When managed strategically, the balance between interest and appreciation tilts decisively in favor of patient, informed owners who view property as both a stable home and a cornerstone investment.